Imagine a neobank that isn’t tied to traditional banks but operates entirely onchain. This once seemed like a futuristic concept, but now it is within reach. The question is—who will be the first to launch a truly non-custodial neobank? Could it be a big bank, an existing neobank, or a completely new player?

Neobanks have revolutionized banking, making it more accessible and user-friendly. However, they’re still tied to the old financial systems they sought to disrupt, which has led to vulnerabilities, as seen with recent issues like Synapse and Evolve Bank freezing thousands of customer accounts. Despite the innovations, these modern fintech companies are still dependent on outdated infrastructure.

As Angela Strange famously said, “Every Company Will be a Fintech Company,” but the transition hasn’t been without friction. At Rehive, we’ve observed how the Banking-as-a-Service (BaaS) model often adds costs and delays. Meanwhile, blockchain networks like Coinbase’s Base are enabling faster development without reliance on traditional banks.

Cryptocurrency adoption has been hindered by currency volatility, high on-chain fees, and a lack of simple financial services expected by consumers. But with the emergence of stablecoins, low-cost transactions, decentralized savings and lending, and Web3 card payments, the technology is now in place to offer everything a neobank does—on the blockchain. This shift is timely, as consumers grow frustrated with inflation and the innovation roadblocks hit by fintechs.

Combining the user-friendly nature of neobanks with the benefits of blockchain, there’s a real opportunity to reinvent banking and overcome the limitations of traditional systems.

The state of neobanking

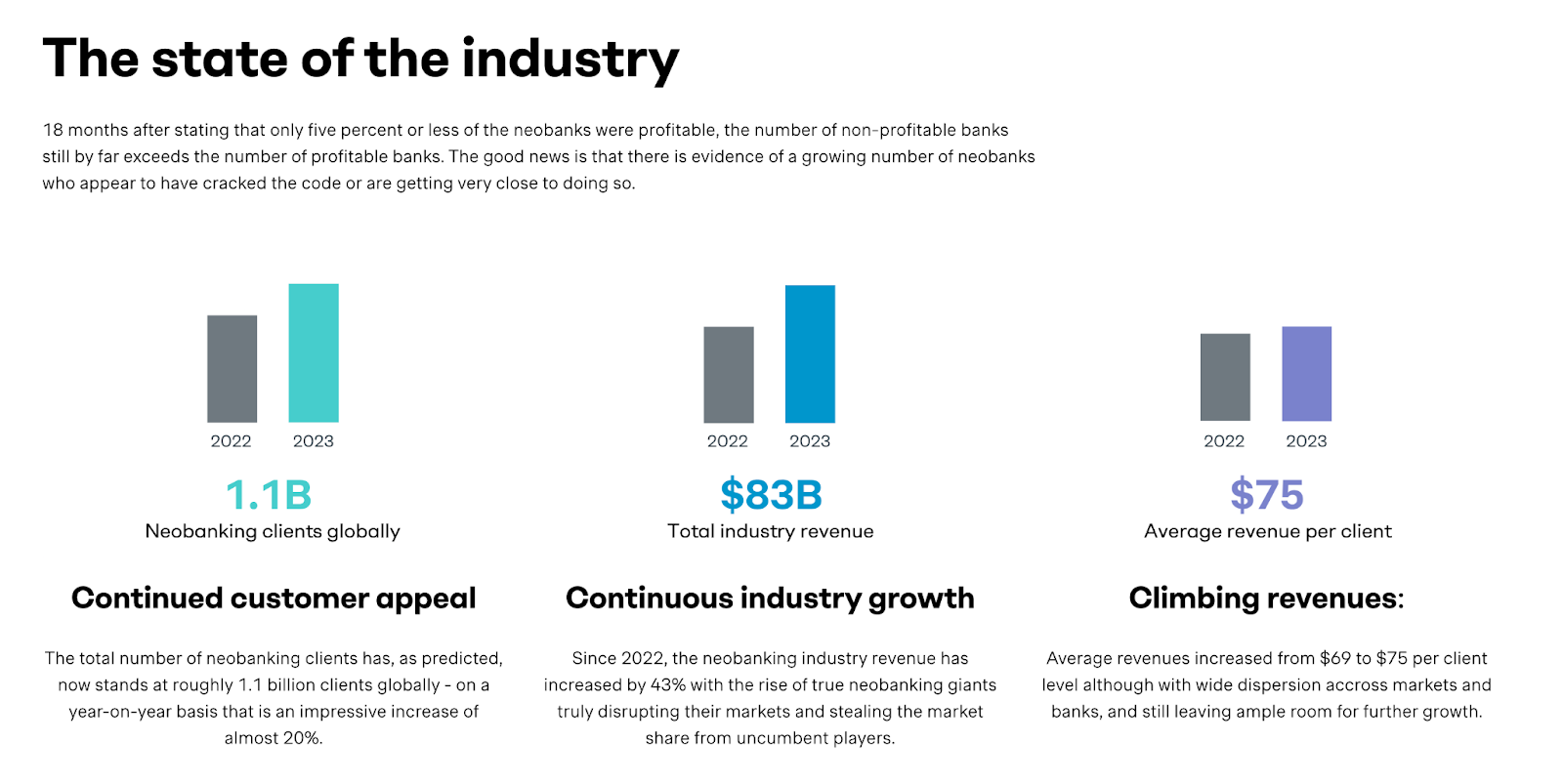

Neobanks are immensely popular, with over 1 billion users as reported by Simon-Kutcher. Companies like NuBank, Revolut, and Monzo have found success by focusing on customer experience and innovative operating models, achieving profitability and generating impressive revenues.

However, the market is facing significant challenges. Regulatory hurdles and economic conditions have slowed the expansion of neobanks in some regions, and profitability remains elusive for many. Further compounding these challenges, research by Simon-Kucher reveals that the pace of new neobank launches is declining, and closures may soon outnumber openings. From January 2022 to July 2023, 36 new neobanks were launched globally, while 34 shut down. In the U.S. alone, eight neobanks opened, but five were forced to close.

The FDIC has recently issued a warning to consumers about the risks of using neobanks and fintech companies for banking services. This caution is particularly relevant as millions of Americans rely on these platforms for their banking needs, yet may not be fully aware of the limitations of FDIC insurance in these contexts.

Non-Custodial wallets and stablecoins

Non-custodial wallets, also known as self-custody wallets, are rising in popularity as they provide users with full control—also referred to as "custody"—over their digital assets. Unlike crypto wallets offered by centralized exchanges, where the provider controls your private keys, non-custodial wallets ensure that only the owner has access to their private keys and, consequently, their assets. This sovereignty allows users to directly interact with decentralized finance (DeFi) protocols, enabling activities like lending, borrowing, and trading without intermediaries.

Robinhood and Coinbase have set a precedent by launching their own Web3 products separate from their main apps, signaling a shift towards providing users with more control over their digital assets. From an innovation perspective, it is easier to develop solutions for non-custodial wallets since they currently benefit from a more flexible regulatory environment in many regions and involve less overhead, as there is no need to custody funds for end users. However, non-custodial wallets are currently more geared towards advanced users, given the responsibility of managing private keys and navigating complex interfaces. That said, newer innovations in user experience (UX) are making these wallets more accessible, setting the stage for broader mainstream adoption.

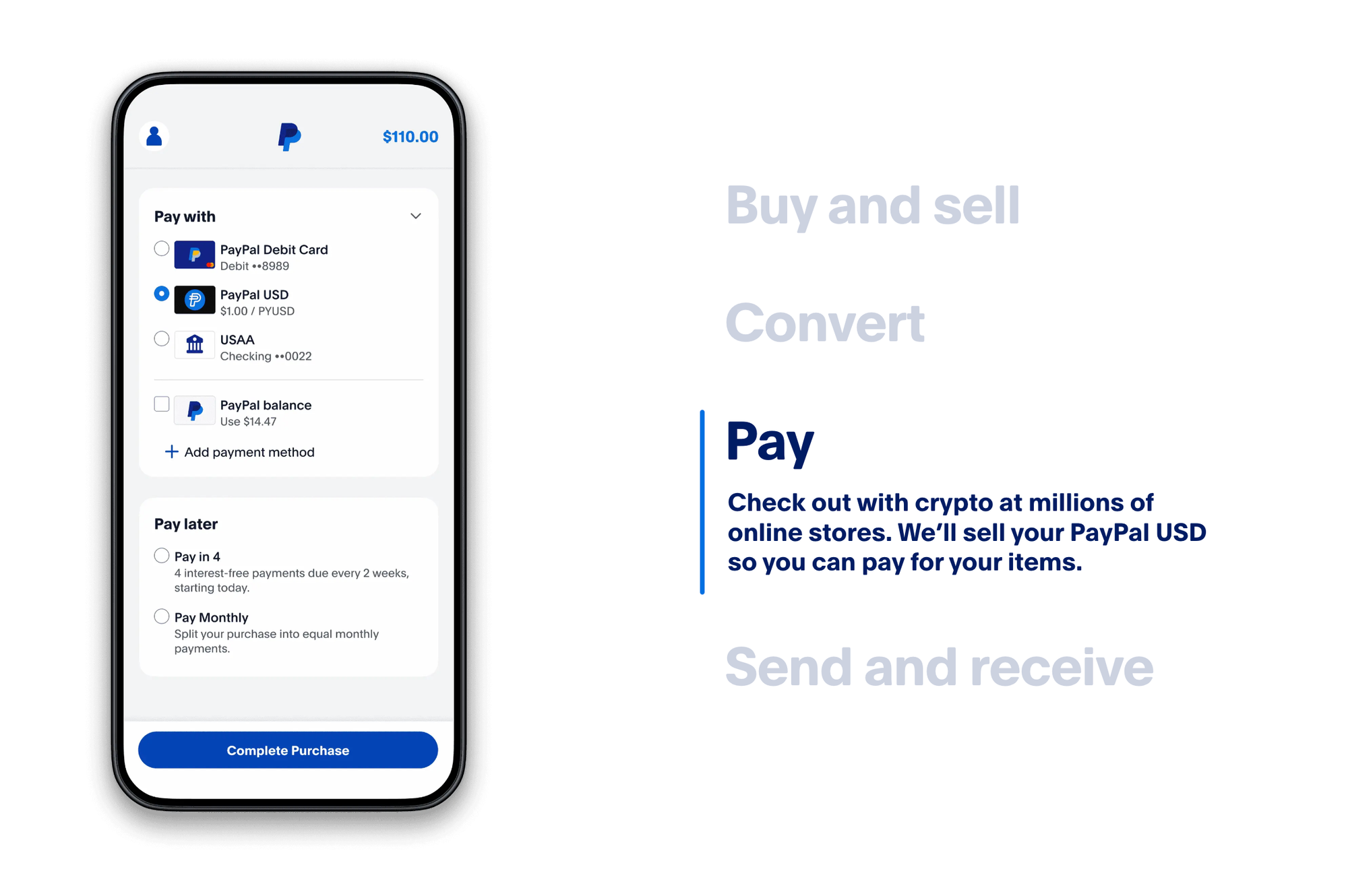

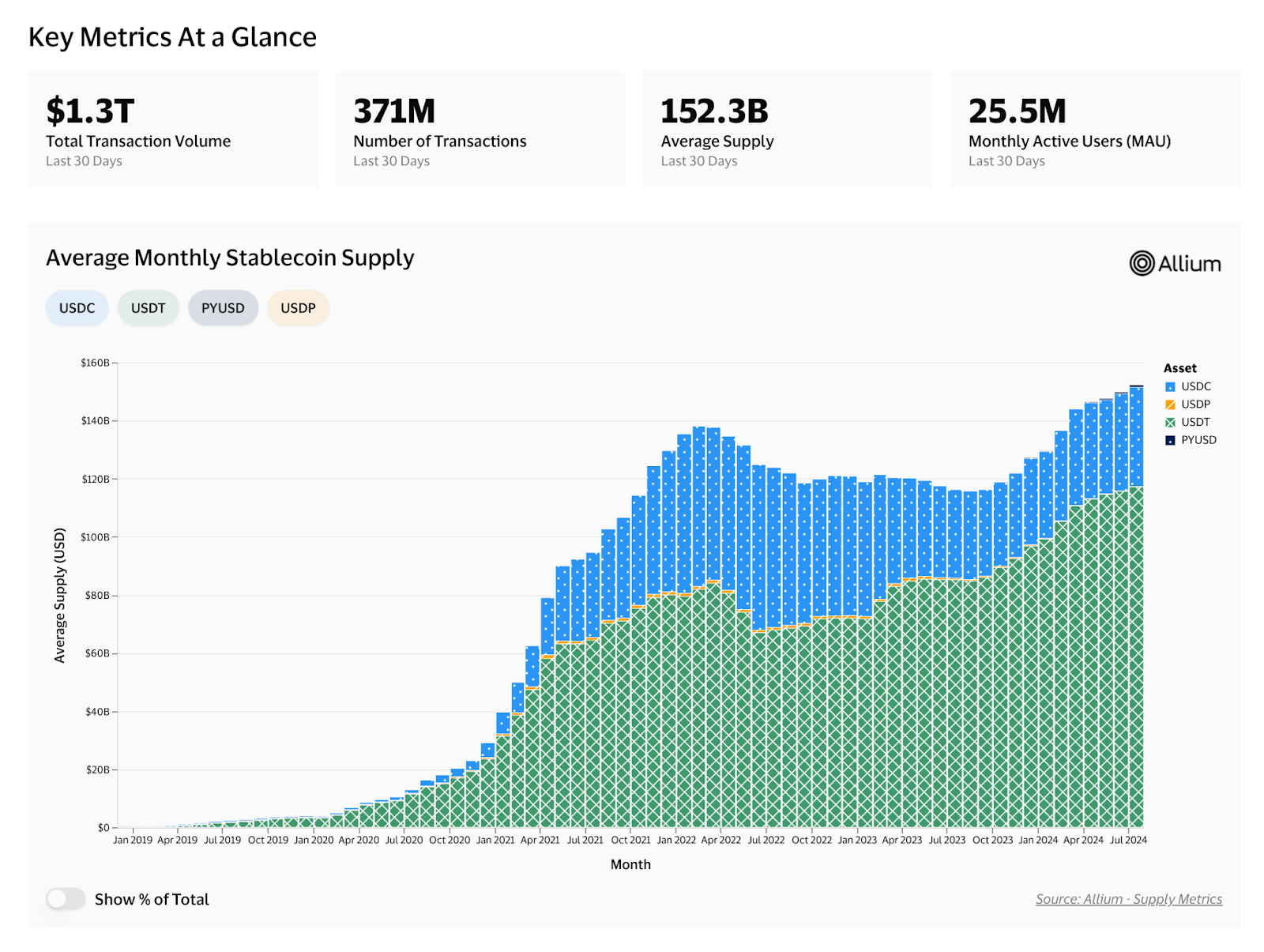

The adoption of stablecoins, like USDC, has filled the gaps that once hindered blockchain’s potential, offering instant global transactions and stable value. In August 2023, PayPal launched its own U.S. dollar-backed stablecoin, PayPal USD (PYUSD), issued on the Ethereum blockchain. This move by PayPal, one of the largest financial technology companies, underscores the growing importance and adoption of stablecoins in global finance.

Visa’s stablecoin portal shows the rapid growth of these assets, with use cases expanding to retail trading in DeFi and cross-border remittances.

Mastercard’s Web3 Card and the future of non-custodial neobanking

Mastercard’s Web3 card is a key innovation, allowing users to spend digital assets while maintaining control over their funds. This advancement, combined with stablecoins and non-custodial wallets, positions non-custodial neobanking as a compelling alternative to traditional models.

Mastercard has been working closely with industry leaders like MetaMask to launch this card program, ensuring that it includes not only the best of blockchain technology but also the robust security features expected from a global payment network. This includes Mastercard’s dispute management process, chargeback protections, and the integration of know-your-customer (KYC) and anti-money-laundering (AML) protocols.

Why now is the perfect time for non-custodial neobanking

- Frustration with BaaS: Traditional Banking-as-a-Service models are causing delays, adding costs, and creating headaches for fintechs.

- Rising stablecoin adoption: Stablecoins are providing a stable value and enabling low-cost global transactions, addressing the volatility that once hindered blockchain adoption.

- Improved usability of self-custody solutions: Non-custodial wallets are becoming more user-friendly, making it easier for users to manage their digital assets.

- Built-In yield opportunities: DeFi protocols are offering yield-generating opportunities, making non-custodial wallets more attractive.

- Low-cost transactions on Layer 2 Networks: Layer 2 solutions are reducing transaction costs, making blockchain-based services more viable.

- Frustration with high inflationary currencies: As inflation erodes the value of traditional currencies, more people are seeking stable, decentralized alternatives.

- Innovations like the Web3 Card: New products, like Mastercard’s Web3 card, are bridging the gap between digital assets and everyday spending.

- Evolving regulatory landscape: Non-custodial wallets currently benefit from a more flexible regulatory environment, which allows for quicker innovation and adaptation to new financial technologies.

Stay ahead with Rehive

Interested in exploring more about the future of non-custodial banking, stablecoins, and DeFi?

Subscribe to our newsletter, where we’ll continue to delve into these opportunities and share insights on how Rehive’s white-label solutions can help you navigate this evolving landscape.