Loading...

FAQs

How can we help you get started?

How can we help you get started?

Helghardt

August 15

We have an exciting update to share! We are working on a white-label multi-chain, self-custodial wallet powering stablecoins and cryptocurrencies. Self-custody has been a key research area within Rehive for the last couple of years, but finally, the stars are lining up to make this possible.

We believe a wave of stablecoin-focused fintechs is emerging and Rehive is well-positioned to be a leading provider. If you are working at an enterprise, bank, or fintech startup and want to learn more, please reach out.

Our close clients and partners know the story—you have been with us every step of the way. In 2016, we decided to build tools that make it easy for other fintechs to launch and scale. We felt that a platform like “Shopify for fintech” was a missing piece in helping new fintechs go to market. Over the years, we have helped over 25 projects successfully launch on Rehive. In the process, we built a powerful fintech platform with ready-made white-label apps and value-added extensions.

Early on, we were interested in stablecoins. In 2014, we explored a stablecoin concept for the Bitcoin blockchain but moved on to found Rehive. At one point, we considered building Rehive on Ethereum but felt that the market we wanted to serve was not ready for pure crypto solutions due to high fees and complex user experiences. In 2017, we started building a closer relationship with Stellar, known for its low-cost network with a focus on real-world use cases. Yet again, it was too early for stablecoins to take off for retail use cases.

We built Rehive to be flexible and open-ended for any kind of fintech use case, without relying on out-of-the-box integrations. Over time, we focused on cloning Cash App-like features for individuals and businesses. Clients had to secure the relevant licenses, custody partners, and on/off ramps in their target regions. Between 2020 and 2022, Bank-as-a-Service (BaaS) began to gain momentum, and we saw an opportunity to offer an end-to-end fintech solution by partnering with Wyre. This was magical—suddenly, clients could go live within days of getting their account approved by Wyre.

Unfortunately, Wyre closed down, and subsequently, a whole wave of BaaS providers followed suit. We learned the hard way that banks are not designed to work at the breakneck speed demanded by fintechs, and somewhere along the way, parties slip up. The worst part is when customers are left stranded with their funds locked up or lost forever. The most recent drama was the shutdown of SynapseFi, an early BaaS provider, along with their bank partner, Evolve Bank.

BaaS is not a complete failure. Providers like Fifth Third Bank, Thread Bank, and Column are forging the way as developer-native banks in the U.S., playing their part in the ecosystem. Unit is also making a significant impact as a full white-label solution for neobanking in the U.S. They have shown that the model can work. However, we believe there is a bigger opportunity to build on-chain solutions with a focus on stablecoins.

Our clients can still integrate with BaaS providers, but we don’t plan to offer this as out-of-the-box integrations.

The BaaS model is inherently unreliable. Too many stakeholders lead to significant compliance overhead, high costs, and painful shutdowns. Additionally, a BaaS provider is often limited to specific countries, meaning that expanding to other regions brings the same challenges all over again.

Non-custodial wallets and stablecoins offer a fundamentally better infrastructure layer for innovation. We aim to be the leading provider in making this a reality for everyday finance use cases.

The three main reasons for self-custodial:

We will share more details about our self-custody architecture in the coming weeks.

Stablecoins offer the benefits of blockchain technology with the stability of fiat currency: programmable money, low-cost, global, and instant payment rails. In our opinion, the best part is the ability to leverage programmable money and a global standard for building on top of. For example, if a fintech app in the U.S. supports stablecoins, it becomes possible to send money directly to a recipient in South Africa if that app also supports stablecoins. This is a great foundation for a fintech platform like Rehive!

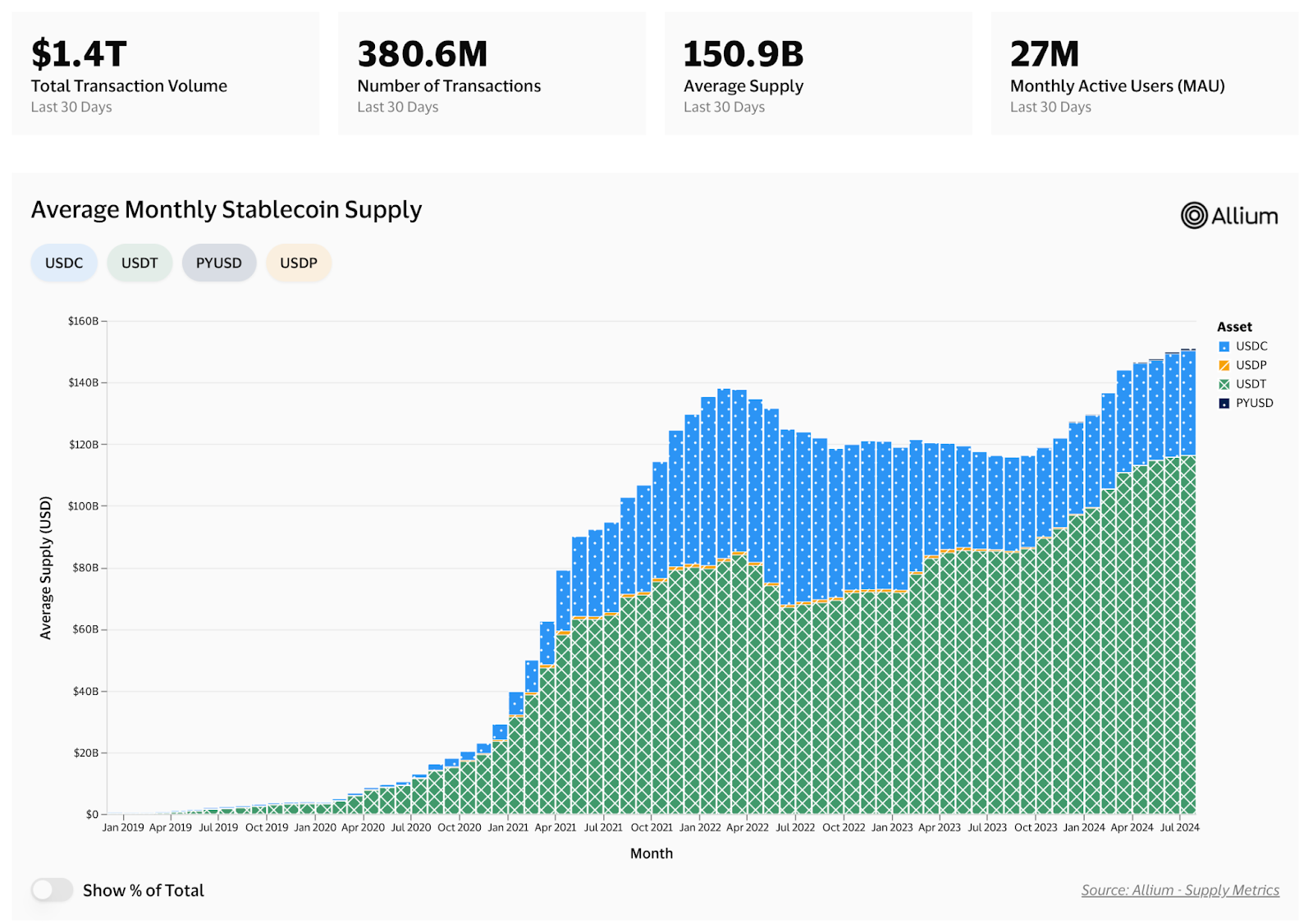

Stablecoin adoption has been growing consistently, with the total supply exceeding $150 billion among the top stablecoins. The screenshot below shows the total supply over the last five years.

Outside of leading stablecoins, issuers are growing in other regions too. Stablecoin Standard is a global industry standard for issuers and features over 15 issuers in different countries.

In the coming weeks, we'll delve deeper into the stablecoin ecosystem, sharing our insights on current trends and explaining why we believe the timing is perfect for this technology to revolutionize fintech.

In the last two years, we have been extremely disheartened by BaaS providers failing and leaving customers stranded. At the same time, the stars are aligning for self-custody stablecoin solutions to become viable!

There has been major progress as more on/off-ramp providers emerge, stablecoins gain traction, acceptance of stablecoins grows, and there have been significant advancements in UX/UI for non-custodial wallets. These wallets now allow users to control their funds while still offering easy recovery options.

Our model remains the same. We help enterprises, banks, and fintech startups launch and scale on Rehive with our ready-made white-label fintech apps. The only difference is that we will now focus on self-custody solutions with pre-integrated on and off-ramps supporting various regions.

Clients will still be able to build on the API or leverage our white-label apps to make codebase-level customizations as needed. It will remain easy to build custom extensions and create unique value-adds for your customers.

Rehive’s off-the-shelf features will also remain the same. We will continue to support web and mobile apps for businesses and individuals. Key features include mass payouts, invoicing, point-of-sale payments, agent top-ups, in-app purchases, payment requests, peer-to-peer payments, conversions, and more.

Depending on who you are, Rehive offers unique benefits:

Heading into 2025, this is the perfect time to be part of bringing the next wave of customers on-chain with friendly, secure, and useful self-custody payment solutions.

We do plan to eventually build our products to demonstrate the value proposition, but we believe existing businesses or local fintechs are better positioned for the following reasons:

Contact us if you are interested in launching a solution for your region.